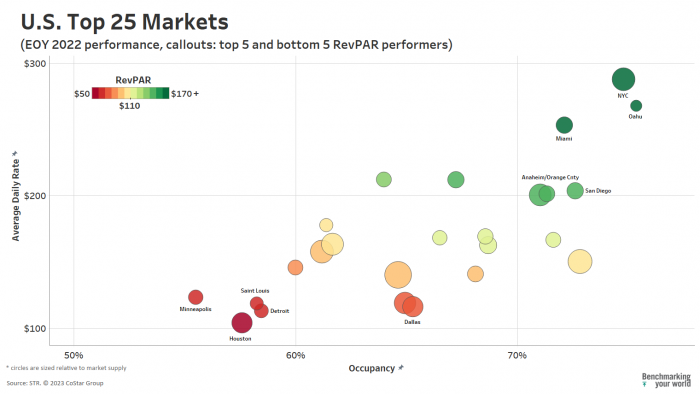

Top-line performance recovery was aplenty around the U.S. in 2022 as record-breaking levels of demand were combined with strong pricing power in an inflationary setting. Among the recovery highlights, New York City made a phenomenal comeback to grab the nation’s top spot in revenue per available room (RevPAR), while smaller hotel destinations with a primary focus on high-end travelers also found significant levels of success for the year.

Overall, New York City’s nominal RevPAR (non-inflation adjusted) for 2022 led the Top 25 Markets at $215. That level was down $4 from 2019 but up 72% year over year. Rounding out the Top 25 Market leaders were Oahu (+61% from 2021 to $202), Miami (+23% to $183) and San Diego (+45% to $148). Even the lowest RevPAR performers from the Top 25 group experienced notably positive lifts from the prior year, including Houston (+20% to $60), Detroit (+25% to $66), Minneapolis (+53% to $68), St. Louis ( +32% to $69) and Dallas (+35% to $76). Demand levels in 2022 were higher than 2019 for six of the Top 25 Markets, including Miami and Dallas.

Compared to 2019, NYC’s total-year performance was down in demand (-13%) and occupancy (-10.1 percentage points) from 2019. However, that end-of-year telling of the market’s performance does not completely reveal (or revel in) New York City’s strong hand in play at end of the year. Starting in April, NYC began to rally from a slow, Omicron-impacted first quarter to take top position among large markets. By September, the Big Apple was in the lead position with real RevPAR of $280, which was driven by an enviable ADR of $345 and a healthy four-month average occupancy of 83.0%. By comparison, the distant second-best large market during that period, Oahu, had $204 RevPAR, $273 ADR, and 73.2% occupancy. A variety of factors contributed to NYC’s fourth-quarter resurgence, including a continued strong showing in domestic leisure demand, but also an influx of international travelers along with the rebooting of business travel to the market.